Tax deductions for charitable contributions have traditionally been an important consideration when developing a financial and tax strategy. But changes brought by the 2017 Tax Cuts and Jobs Act and further solidified with the One Big Beautiful Bill Act require donors to take a more strategic approach to utilizing the charitable contributions through itemized deductions because the higher standard deduction it instituted reduced the likelihood that donors could benefit from itemization.

With a little planning, you can continue giving charitably while maximizing tax savings. Whether you use a donor-advised fund, such as T. Rowe Price Charitable, or donate directly to your favorite charity, here are a few ideas to consider.

Four strategies for tax-smart giving

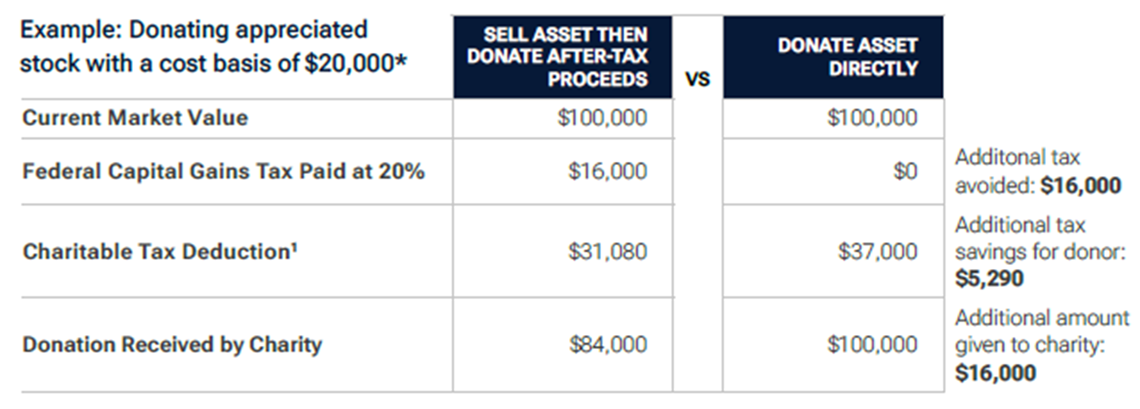

1. Donate long-term appreciated assets

Do you have appreciated assets you want to sell, such as stocks, bonds, mutual funds, real estate, business interests, collectibles, or even cryptocurrency? If so, you may want to determine whether cashing out or taking a tax deduction would be more favorable. Whatever kind of asset you consider donating, the accompanying illustrations demonstrate how that asset could result in significant support for your favorite charities.

This is an illustration for donating appreicated, unrestricted, marketable stock held for more than 1 year to a public charity (including a donor-advised fund).

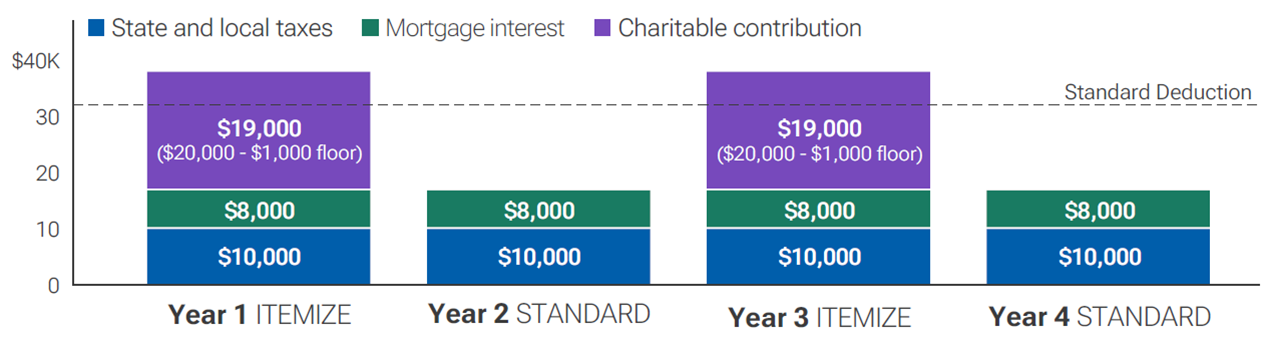

2. Bunch up: Group your giving to qualify for itemized deductions

With a higher standard deduction after the recent tax law changes, many taxpayers are unable to benefit from itemized deductions. A strategy called bunching enables you to realize tax savings from itemization once again. Rather than make yearly charitable contributions, combine two or more years of contributions into one tax year to increase your itemized deductions for the year above the applicable standard deduction. Then, for the following year(s) already covered by the bunching, you would take the standard deduction. And if you use T. Rowe Price Charitable, you can continue to disburse grants to charities annually, even when bunching contributions into your giving account.

Example: How bunching works for the Palmer family

The Palmers have an adjusted growth income (AGI) of $200,000 and pay $8,000 in mortgage interest and $10,000 in state and local taxes. There is a .5% floor on charitable contributions, which is $1,000 for the Palmers. By doubling their yearly $10,000 charitable contribution in Year 1 and Year 3, they exceed the $32,200 standard deduction.2 Thus, the Palmers increase their deductible expenses above the standard deduction by $4,800 for Year 1 and a similar amount for Year 3.

3. Minimize capital gains tax when rebalancing your portfolio

When investors rebalance their investment portfolios to ensure that their asset allocation is aligned with their long-term goals, they may sell both winners and losers in the process. The rebalancing may leave you with more gains that are not fully offset by losses. If you can benefit from itemizing your deductions, you can donate some of the appreciated securities you would otherwise sell to avoid taxes on capital gains and benefit from the charitable tax deduction. You should be mindful of the deduction limitations due to your adjusted gross income or the type of charities you are donating to. Consult IRS Publication 526 or your tax advisor if necessary.

4. Start a giving account before you retire

If you are nearing retirement, consider opening a T. Rowe Price Charitable account. Then fund it generously while your income and tax bracket are still high and you are likely eligible for the charitable tax deduction. This ensures that you have ample resources to support your favorite charities in retirement (when your financial resources may be constrained) but have more time to focus on philanthropy. And there is another benefit of this strategy—any growth on your invested giving account is tax-free.

Use our calculator to estimate your tax savings..

Bunch your giving and boost your tax savings.

1 The Federal income tax benefit is calculated at 37% assuming that you can fully realize the federal income tax benefit from itemizing your deductions. This also assumes that other charitable contributions exceed the floor of 0.5% of adjusted gross income effective in 2026. Your savings may be reduced due to the amount of your adjusted gross income or if your donation is not made to a public charity. This illustration does not take into account your state or local taxes or the 3.8% Medicare surtax, which may result in additional tax savings. Savings in all cases could be significantly reduced if your donated asset is subject to restrictions or has a holding period of 1 year or less.

2 The standard deduction is $32,200 for 2026 for married couples filing jointly and adjusts annually for inflation. This example assumes the annual standard deduction for married couples filing jointly is consistently $32,200.

All investment pools are subject to risk including the possible loss of principal.

T. Rowe Price Charitable is an independent, nonprofit corporation and donor-advised fund founded by T. Rowe Price to assist individuals with planning and managing their charitable giving.

© 2026 The T. Rowe Price Program for Charitable Giving, Inc. All rights Reserved. T. ROWE PRICE, INVEST WITH CONFIDENCE, the BighornSheep design, and related indicators are trademarks of T. Rowe Price Group, Inc. All other registered trademarks and service marks are the property of their respective owners

- 5217353